Rental Property Carpet Depreciation Rate

A Property Inventory Template Is The Record Of A Rental Property And All Its Contents The Schedule Of Conditi Templates Printable Free Template Free Templates

Rental Property Deduction Checklist For Landlords Bradstreet Cpas Tax Tip Of The Week

The Irs S Dirty Little Secret About Rental Properties By Becky Harding Medium

Rental Property Calculator Calculate P L Schedule

Depreciable Life Life Expectancy For Rental Purchases

Residential Rental Property Depreciation Calculator

Instead use form 2106.

Rental property carpet depreciation rate.

Best Flooring For Rental Property Updated For 2019 Rentprep

Rental Property Tax Deductions Property Tax Deduction

Paying Back Depreciation On A Rental Property Home Guides Sf Gate

What Is Rental Property Depreciation And How Does It Work

Do You Understand Income Tax Considerations Of Rental Properties Rental Property Investment Rental Property Rental Property Management

Flooring For Rental Properties All You Need To Know

Inventory Template For Furnished Rental Property Word Template Budget Spreadsheet Template Being A Landlord

2018 Tax Laws That Affect Real Estate We Will Guide You Through The Sales Process Consult Your Cpa For Det Investment Property Estate Tax Real Estate

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

Buying Your First Rental Property Ultimate Guide Learn How To Buy A Rental And Create Passive Income

How To Deduct Rental Property Depreciation Wealthfit

15 Gif 735 550 Https 75maingroup Com Rent Agreement Format Being A Landlord Rental Property Management Property Management

A Landlord Inventory Template Is A List Of Everything That Your Landlord Provides With The Property You Rent Being A Landlord Free Word Document Word Template

Residential Rental Property Taxes Bradley Smith Inc

The Basics Of Depreciation For Real Estate Rental Property El Dorado Hills Bookkeeping

Everything You Need To Know About Depreciation On Rental Property Investment Property Tips Mashvisor Real Estate Blog

Rental Property Repairs Vs Improvements Tellus Talk

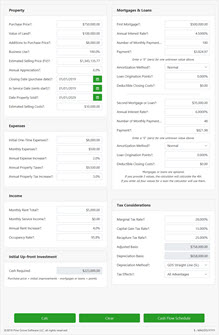

1

Rental Property Income What To Report And What To Deduct On Your Taxes The Official Blog Of Taxslayer

10 Tax Deductions For Smart Investors Passive Real Estate Investing Real Estate Investing Flipping Real Estate Investor Real Estate Information

The Advantages Of Owning A Rental Property David Preston Shoes

Video How To Maximize Rental Property Depreciation

Rental Property Tax Deductions Maximize Your Tax Benefits

Source : pinterest.com